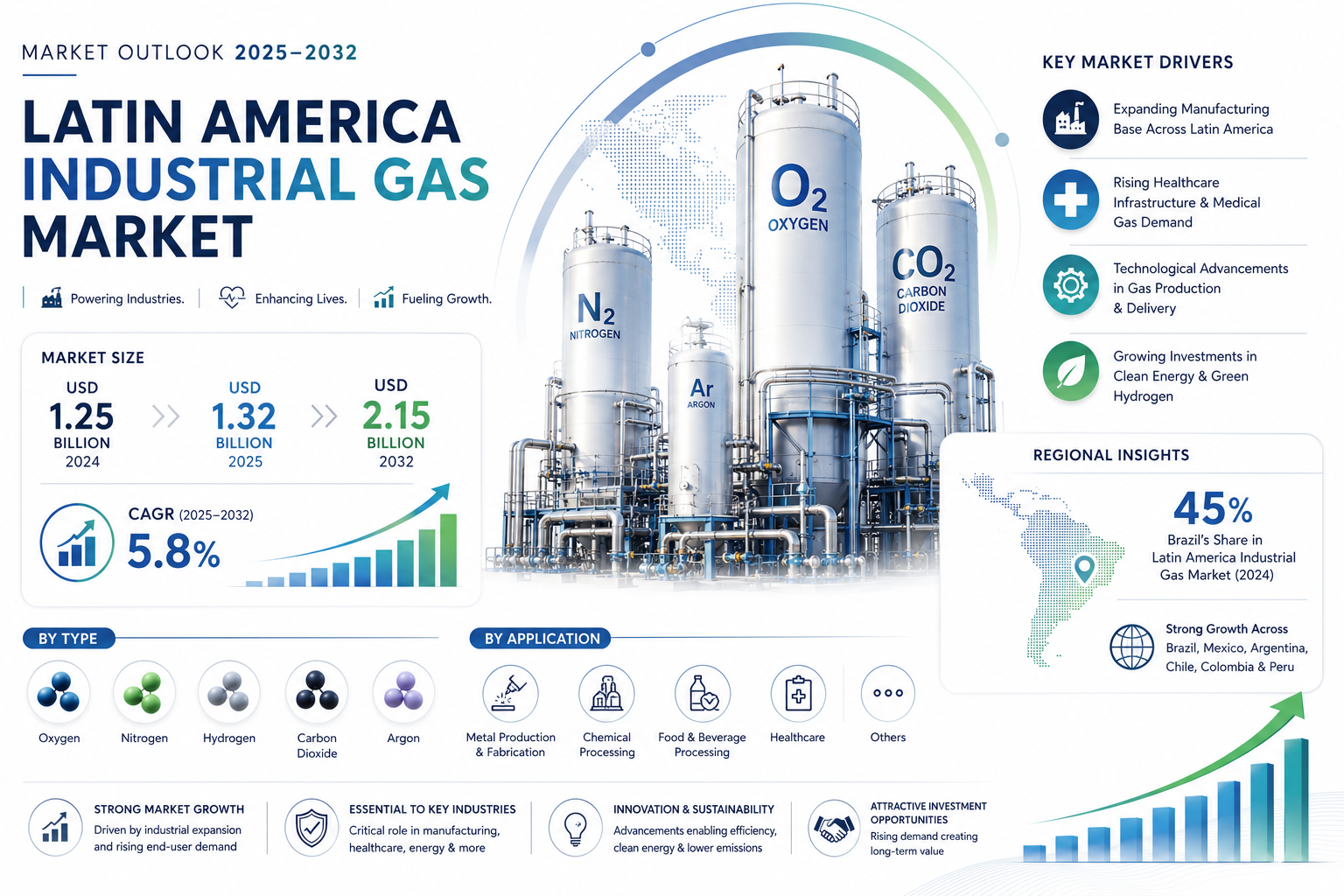

The Latin America Industrial Gas Market size was valued at USD 1.25 billion in 2024. The market is projected to grow from USD 1.32 billion in 2025 to USD 2.15 billion by 2032, exhibiting a CAGR of 5.8% during the forecast period.

Industrial gases are essential chemical substances produced for use across manufacturing, healthcare, energy and other industrial applications. These gases - including oxygen, nitrogen, hydrogen, carbon dioxide and argon - are manufactured through air separation, steam reforming and other production methods. They serve critical functions from metal fabrication to medical therapies, with purity levels and delivery methods tailored to specific industry requirements.

Market growth is driven by expanding manufacturing sectors across Latin America, particularly in Brazil and Mexico, along with increasing healthcare infrastructure development. The post-pandemic emphasis on medical oxygen capacity and the region's growing metal production industry are creating sustained demand. Major players like Linde and Air Liquide continue investing in production facilities, with Brazil accounting for 45% of regional industrial gas consumption as of 2024.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/286563/latin-america-industrial-gas-market

Market Overview & Regional Analysis

Brazil stands as the undisputed leader in the Latin America industrial gas market, representing the largest and most mature market in the region. Its dominance is driven by a vast and diversified industrial base, particularly within the manufacturing and healthcare sectors, which are the largest consumers of industrial gases. The country's well-established infrastructure for production, including advanced air separation units, and a robust distribution network ensures a steady and reliable supply to key industries such as automotive, metallurgy, food processing, and pharmaceuticals. Major global industrial gas corporations have a significant and deeply integrated presence in Brazil, investing heavily in local production facilities and technological advancements. The continuous expansion of the healthcare sector, especially following heightened demand for medical gases post-pandemic, further solidifies Brazil's leading position. Ongoing infrastructure projects and industrial growth initiatives by the government are expected to sustain this market leadership.

Brazil's extensive industrial sector, including major automotive, chemical, and steel industries, creates a consistent and high demand for a wide range of industrial gases like oxygen for metal fabrication and nitrogen for creating inert atmospheres in chemical processes. This strong industrial foundation is a primary driver of its market leadership. The country's large and evolving healthcare infrastructure is a significant consumer of medical-grade gases, particularly oxygen. High demand from hospitals and clinics, coupled with government focus on improving healthcare access, ensures a steady and growing market for industrial gas suppliers within this critical sector. Brazil possesses the most developed infrastructure for industrial gas production and distribution in Latin America. Significant investments by leading international companies have resulted in a network of efficient air separation plants and logistics systems, enabling reliable supply even to remote industrial centers. As the economic powerhouse of South America, Brazil serves as a strategic hub for industrial gas companies operating across the region. Its market size and sophistication often dictate regional trends and attract continued investment in new technologies and applications for industrial gases.

Mexico represents the second-largest market for industrial gases in Latin America, heavily influenced by its strong manufacturing sector, particularly the automotive and aerospace industries which are deeply integrated with North American supply chains. The demand for gases such as argon for welding and nitrogen for blanketing is substantial. The country's growing food and beverage processing industry also contributes significantly to the consumption of carbon dioxide and nitrogen. Proximity to the United States facilitates technology transfer and investment, though the market also faces challenges related to economic volatility and regulatory complexities. The energy sector presents a growing area of opportunity for industrial gases, particularly hydrogen.

Argentina's industrial gas market is characterized by its significant agricultural and energy sectors, which drive demand for specific gases. The food and beverage industry, a major exporter, utilizes large volumes of carbon dioxide and nitrogen for freezing, packaging, and carbonation. The country's vast natural gas reserves also underpin a growing petrochemical industry, creating demand for hydrogen and other process gases. However, the market's growth is often tempered by economic instability and fluctuating industrial output. Despite these challenges, there is potential for growth in medical gases and applications related to renewable energy and sustainability initiatives.

Chile's industrial gas market is closely tied to its dominant mining industry, one of the largest in the world. This sector creates robust demand for oxygen in mineral processing and explosives, and for nitrogen in inerting applications. The country's stable economy and pro-business environment attract investment, supporting market development. Furthermore, Chile's advanced fruit export industry drives consumption of gases for controlled atmosphere storage and packaging. The market is also seeing increasing interest in gases for environmental applications, such as water treatment and renewable energy projects, aligning with the country's strong focus on sustainability.

Colombia and Peru are emerging markets within the Latin American landscape, showing promising growth potential. Both countries are experiencing industrial diversification and infrastructure development. In Colombia, the manufacturing, food processing, and oil and gas sectors are key consumers. Peru's market is similarly driven by its robust mining industry, demanding oxygen and nitrogen, alongside a growing food and beverage sector. While their markets are smaller than regional leaders, increasing foreign investment and economic stability are fostering a more favorable environment for the expansion of industrial gas applications and infrastructure.

Key Market Drivers and Opportunities

The Latin American industrial sector is experiencing accelerated growth, particularly in manufacturing and energy, creating robust demand for industrial gases. Automotive production in Brazil and Mexico has rebounded strongly, with output increasing by nearly 8% in 2024 compared to the previous year. This resurgence directly correlates with higher consumption of shielding gases for welding and specialty gases for manufacturing processes. Furthermore, the region's metal fabrication sector, which accounts for 22% of industrial gas consumption, continues to expand as infrastructure projects gain momentum.

Post-pandemic healthcare infrastructure development has created sustained demand for medical gases across Latin America. Brazil alone has added over 5,000 new hospital beds since 2021, while Mexico's healthcare expenditure is projected to grow at 6.8% annually through 2032. This expansion requires substantial volumes of medical-grade oxygen, nitrous oxide, and other therapeutic gases. The region's aging population, growing at 3.2% annually, further amplifies this demand as respiratory therapies become more prevalent.

Innovations in air separation technology are revolutionizing gas production efficiency in the region. Modern cryogenic plants now achieve energy efficiencies up to 15% higher than previous generations, significantly reducing operational costs. Membrane technology adoption has grown by 22% since 2020, particularly for nitrogen generation in food packaging applications. These advancements enable suppliers to meet the exacting purity requirements of semiconductor manufacturing and pharmaceutical production, sectors experiencing rapid growth in northern Mexico and southern Brazil.

Latin America's renewable energy sector presents significant growth avenues for industrial gas providers. Green hydrogen projects in Chile and Colombia are expected to require over 150,000 tons of hydrogen annually by 2028. Brazil's ethanol industry is adopting carbon capture technologies that utilize specialized gas mixtures. These emerging applications could add $450 million to the regional market by 2030.

IoT-enabled cylinder tracking systems are revolutionizing inventory management, reducing waste by up to 18% in pilot programs. Cloud-based monitoring of bulk storage installations is becoming standard practice, with adoption rates exceeding 40% among large industrial users. This digital transformation creates opportunities for value-added services and predictive maintenance solutions.

Mexico's burgeoning semiconductor industry requires ultra-high purity gases for fabrication processes. While currently accounting for just 5% of the market, this segment is growing at 23% annually. Investments in display panel production in Brazil are also driving demand for specialty gas mixtures used in thin-film deposition and etching processes.

Challenges & Restraints

Establishing industrial gas production facilities requires substantial upfront investment, with mid-sized air separation units costing between $50-$75 million. This financial barrier prevents smaller players from competing effectively, maintaining the dominance of multinational corporations. Energy costs, accounting for nearly 60% of production expenses, remain volatile across the region, with Brazil experiencing electricity price fluctuations of up to 30% annually.

Divergent regulations between Latin American nations complicate market operations. While Brazil follows strict ANVISA standards for medical gases, Argentina's ENARCOM standards differ significantly in testing requirements. These inconsistencies force manufacturers to maintain multiple production lines, increasing costs by an estimated 12-18%. Customs procedures for cylinder transportation between countries can add up to 14 days to delivery timelines, hindering just-in-time supply models.

Currency fluctuations in Argentina and Venezuela create pricing challenges, with some customers delaying purchases during periods of high inflation. The Brazilian industrial sector's cyclical nature leads to demand swings of up to 20% between peak and trough periods. These economic uncertainties discourage long-term investments in capacity expansion, despite the market's growth potential.

Many industrial centers in the Andean region and Amazon basin lack reliable road networks for cylinder delivery. Transportation costs in these areas can be 35-40% higher than in urban centers, making gas supply economically challenging. Some mining operations in Peru have resorted to on-site nitrogen generation due to these logistical constraints.

The region faces a shortage of technicians trained in handling advanced gas blending and purification systems. Certification programs for medical gas handlers meet only about 65% of market needs. This skills gap slows the adoption of cutting-edge applications in healthcare and electronics manufacturing.

Dependence on imported compressor components and cryogenic equipment creates supply risks. Lead times for specialty valves and heat exchangers have extended to 9-12 months in some cases. These disruptions impact plant commissioning schedules and maintenance operations, potentially delaying capacity expansions.

Market Segmentation by Type

● Oxygen

● Nitrogen

● Hydrogen

● Carbon Dioxide

● Argon

Oxygen is the dominant segment due to its critical applications across multiple high-growth industries. Its essential role in medical therapies, particularly for respiratory care in hospitals, creates steady, non-discretionary demand. Furthermore, oxygen is heavily utilized in Latin America's expanding metallurgy and metal fabrication sectors for cutting, welding, and smelting processes, solidifying its market leadership.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/286563/latin-america-industrial-gas-market

Market Segmentation by Application

● Metal Production & Fabrication

● Chemical Processing

● Food & Beverage Processing

● Healthcare

● Others

Metal Production & Fabrication represents the leading application segment, driven by the region's ongoing industrial development. The use of industrial gases in steelmaking, welding, and metal cutting is fundamental to infrastructure projects and manufacturing output. This segment's robust demand is further supported by growth in the automotive and construction industries, which are key pillars of the Latin American economy.

Market Segmentation and Key Players

● Linde plc (Ireland)

● Air Liquide (France)

● Air Products and Chemicals, Inc. (U.S.)

● Praxair Technology, Inc. (U.S.)

● INFRA S.A. de C.V. (Mexico)

● White Martins Gases e Equipamentos Industriais Ltda (Brazil)

● AGA S.A. (Part of Linde, Argentina)

● Indura S.A. (Part of Linde, Chile)

● Cristol Gas (Chile)

● Tropigas de Colombia S.A. (Colombia)

Report Scope

This report presents a comprehensive analysis of the global and regional markets for Industrial Gas, covering the period from 2025 to 2032. It includes detailed insights into the current market status and outlook across various regions and countries, with specific focus on:

● Sales, sales volume, and revenue forecasts

● Detailed segmentation by type and application

The report features in-depth competitive intelligence including:

● Market share analysis of leading manufacturers

● Production capacity expansions

● Product portfolio assessments

● Strategic partnership evaluations

Our research methodology combines primary interviews with industry leaders and comprehensive data analysis of:

● Production facilities and their geographical distribution

● Raw material sourcing patterns

● End-user industry consumption trends

● Regulatory impact assessments

Get Full Report Here: https://www.24chemicalresearch.com/reports/286563/global-aluminum-plate-sheet-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

● Plant-level capacity tracking

● Real-time price monitoring

● Techno-economic feasibility studies

With a dedicated team of researchers possessing over a decade of experience, we focus on delivering actionable, timely, and high-quality reports to help clients achieve their strategic goals. Our mission is to be the most trusted resource for market insights in the chemical and materials industries.

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/