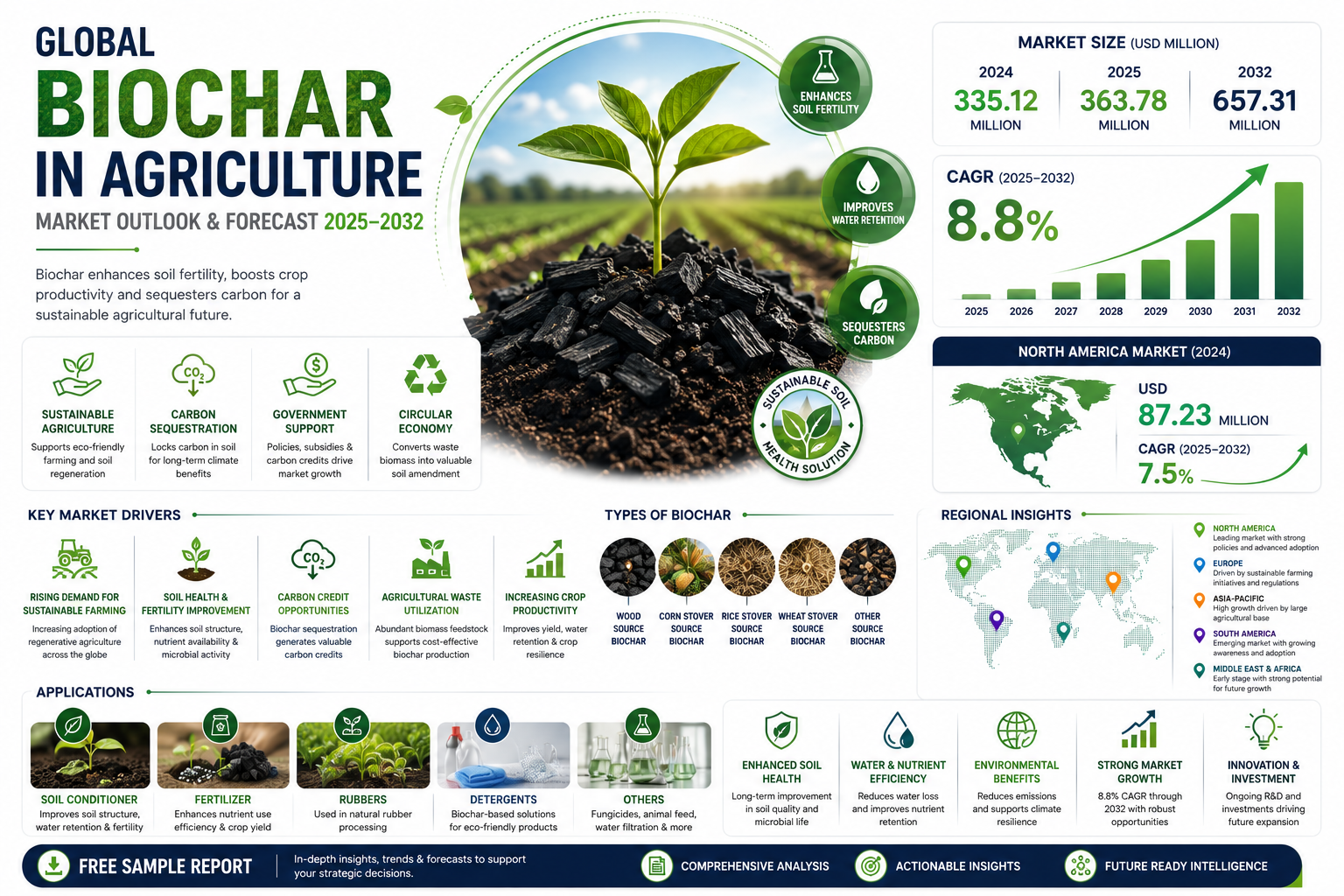

Global Biochar in Agriculture market size was valued at USD 335.12 million in 2024. The market is projected to grow from USD 363.78 million in 2025 to USD 657.31 million by 2032, exhibiting a CAGR of 8.8% during the forecast period. North America accounted for USD 87.23 million of the global market in 2024, growing at a 7.5% CAGR through 2032.

Biochar is a carbon-rich soil amendment produced through pyrolysis of organic biomass such as wood waste, agricultural residues and manure. This highly porous material enhances soil fertility by improving water retention, nutrient availability and microbial activity. Unlike traditional charcoal, biochar is specifically engineered for agricultural applications with optimized surface area and chemical properties.

The market growth is driven by increasing adoption of sustainable farming practices and carbon sequestration initiatives. Government programs promoting soil health management, particularly in the US and EU, are accelerating commercial adoption. Key players are expanding production capacity to meet growing demand - in March 2024, CarbonCycle LLC announced a $20 million investment in new pyrolysis facilities across Midwestern US farms.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/284790/global-regional-biocharagriculture-forecast-supply-dem-analysis-competitive-market

Market Overview & Regional Analysis

North America is recognized as the leading market for biochar in agriculture, driven by a confluence of strong regulatory support, advanced agricultural practices, and high awareness of sustainable soil management. The region benefits from substantial investment in research and development, fostering innovations in pyrolysis technologies and biochar application methods. The presence of a robust organic farming sector and a growing consumer preference for sustainably produced food create a consistent demand. Supportive government policies and carbon credit initiatives further incentivize adoption, positioning the market for significant growth as farmers increasingly seek climate-resilient and productivity-enhancing soil amendments.

The US and Canadian governments actively promote biochar through agricultural subsidies and environmental regulations aimed at carbon sequestration. Policies encouraging the use of organic soil amendments and participation in carbon markets provide a strong foundation for market expansion, making it attractive for both producers and farmers. Significant investments in agricultural research institutions and private companies drive the development of high-quality, tailored biochar products. This focus on innovation ensures effective integration into modern farming systems, enhancing crop yields and soil health, which is a key factor in the region's leadership. A well-established market for organic produce creates natural demand for biochar as a key input for soil conditioning. Farmers are increasingly adopting sustainable practices, viewing biochar as a long-term solution for improving soil fertility and structure without relying on chemical fertilizers. North America has a mature supply chain for biochar production and distribution, with numerous established manufacturers and a network of agricultural suppliers. This logistical advantage ensures consistent product availability and support services for farmers, facilitating broader adoption across the continent.

The European market for biochar in agriculture is characterized by stringent environmental regulations and a strong focus on the circular economy. The European Union's Green Deal and Farm to Fork strategy emphasize sustainable agricultural practices, creating a favorable environment for biochar adoption. Countries like Germany, France, and the UK are at the forefront, with research focused on integrating biochar into organic farming and waste management systems. The market growth is further supported by initiatives that promote carbon farming, where biochar plays a crucial role in sequestering carbon and improving soil health, aligning with the region's ambitious climate targets.

The Asia-Pacific region represents a high-growth market with immense potential, driven by large agricultural sectors in countries like China and India. The primary drivers include the need to address soil degradation, improve crop yields, and manage agricultural waste efficiently. Government initiatives promoting sustainable agriculture and growing awareness of biochar's benefits are key factors. However, market development varies significantly, with more advanced adoption in countries with stronger research infrastructure and government support, while others are still in the early stages of exploration and pilot projects.

In South America, the biochar market is emerging, with growth primarily fueled by the region's extensive agricultural industry, particularly in Brazil and Argentina. The focus is on using biochar to rehabilitate degraded soils, especially those affected by intensive farming. The availability of abundant biomass feedstock from agricultural residues presents a significant opportunity for local biochar production. Market growth is gradually gaining momentum as awareness increases and pilot projects demonstrate the benefits for soil health and productivity in key cash crops like soybeans and sugarcane.

The Middle East and Africa region is in the nascent stages of biochar adoption in agriculture. Market dynamics are influenced by challenges such as water scarcity and soil aridity, where biochar's water retention properties are particularly valuable. Pilot projects, often supported by international organizations, are exploring its use for desert greening and improving agricultural resilience. Growth is expected to be gradual, reliant on increased awareness, technological transfer, and the development of local production capabilities to make biochar a viable solution for sustainable farming in the region.

Key Market Drivers and Opportunities

The global shift toward sustainable agricultural practices is driving significant growth in the biochar market, with projections indicating the market will reach $557.46 million by 2030. Biochar's ability to enhance soil fertility while sequestering carbon aligns perfectly with modern farming's environmental priorities. Agricultural sectors in North America and Europe are leading this transition, with organic farming acreage increasing by 11% annually since 2020. The amendment's unique porous structure improves water retention by up to 18% and nutrient availability by 25-30%, making it particularly valuable in drought-prone regions.

Government initiatives to combat climate change are accelerating biochar adoption through carbon credit programs and agricultural subsidies. The European Union's updated Common Agricultural Policy now includes biochar applications as eligible for green farming subsidies, with over €120 million allocated for biochar projects through 2027. In the United States, the 2024 Farm Bill provisions include tax incentives for carbon-negative farming practices, with biochar qualifying for up to $40 per ton of carbon sequestered. These policies are driving commercial-scale adoption, with over 500 agricultural operations in California alone implementing biochar systems since 2023.

Recent research indicates biochar-amended soils can store carbon for centuries while increasing crop yields by 12-15% compared to conventional methods.

Forward-thinking agricultural suppliers are developing value-added biochar products that address specific farming challenges. Fertilizer manufacturers now offer pre-mixed biochar-blended organic fertilizers that simplify application while boosting efficacy. These premium products command 30-40% higher margins than conventional options, creating new market segments. One leading producer recently launched a biochar seed coating that improves germination rates by 15-20%, demonstrating the technology's versatility beyond soil amendment applications.

The expansion of regulated carbon markets presents a transformative opportunity for biochar producers. Verified biochar carbon credits currently trade at $75-$150 per ton of sequestered CO2, providing farm operations with new revenue streams. Two major agricultural carbon programs launched in 2024 specifically include biochar protocols, with enrollment growing at 200% annually. Producers that can demonstrate standardized, verifiable carbon sequestration through biochar applications stand to benefit from this emerging financial mechanism.

Challenges & Restraints

Despite its benefits, the biochar market faces significant barriers in production economics. Commercial-scale pyrolysis units require capital investments of $500,000 to $2 million, putting them out of reach for most small and mid-sized farms. Transportation costs add another layer of expense, with bulk biochar costing $80-$120 per ton delivered—nearly double the price of conventional fertilizers in many markets. These economic factors currently limit adoption to large-scale commercial operations and government-funded projects, restricting market penetration to just 8% of potential agricultural applications.

The specialized application requirements for biochar present another challenge. Optimal results require precise soil integration at rates between 5-50 tons per hectare, depending on soil type and crop selection. Most agricultural extension services lack trained personnel to advise farmers on proper application techniques, leading to inconsistent results in early adoption cases. This knowledge gap has slowed adoption rates despite the product's potential benefits.

The lack of universal quality standards for agricultural-grade biochar presents significant market challenges. Testing reveals that products labeled as biochar vary widely in carbon content (30-90%), pH levels (4-11), and contaminant levels. These variations lead to unpredictable field performance, damaging the technology's reputation among early adopters. While the International Biochar Initiative has established guidelines, only 12% of producers currently comply with full certification requirements, slowing professional market development.

Many promising biochar feedstocks fall into regulatory gray areas regarding waste classification. Agricultural byproducts like nut shells and crop residues often face ambiguous transport and processing regulations across jurisdictions. One producer reported spending 18 months navigating permitting for a wood waste pyrolysis facility, highlighting the bureaucratic hurdles facing industry expansion. Clearer regulatory pathways for sustainable waste-to-biochar operations could unlock significant production capacity.

Market Segmentation by Type

● Wood Source Biochar

● Corn Stover Source Biochar

● Rice Stover Source Biochar

● Wheat Stover Source Biochar

● Other Source Biochar

Wood Source Biochar is widely considered the established and high-quality segment, prized for its consistent physical properties, high carbon content, and stable structure, which are ideal for long-term soil amendment. Its dominance is driven by the abundance of forestry residues and wood waste streams, creating a readily available and reliable feedstock. Producers and farmers prefer this type for its predictable performance in improving soil water retention and providing a habitat for beneficial soil microbes, making it a cornerstone product in the market.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/284790/global-regional-biocharagriculture-forecast-supply-dem-analysis-competitive-market

Market Segmentation by Application

● Soil Conditioner

● Fertilizer

● Others

Soil Conditioner stands out as the most prominent application, forming the primary use case for biochar. Its ability to significantly enhance soil health by improving porosity, aeration, and water-holding capacity is the key driver. This application is fundamental for rehabilitating degraded soils and boosting crop resilience to drought, which resonates strongly with sustainable farming practices. While its use as a fertilizer carrier is growing, the core value proposition remains its unparalleled contribution to building long-term soil organic matter and fertility, securing its leading position.

Market Segmentation and Key Players

● Cool Planet (USA)

● Biochar Supreme (USA)

● NextChar (USA)

● Terra Char (USA)

● Carbon Gold (UK)

● ElementC6 (USA)

● Swiss Biochar GmbH (Switzerland)

● Pacific Biochar (USA)

● Biochar Now (USA)

● The Biochar Company (TBC) (USA)

● BlackCarbon (Denmark)

● Carbon Terra (Germany)

● Terra Humana (Poland)

● Liaoning Jinhefu Group (China)

● Hubei Jinri Ecology-Energy (China)

Report Scope

This report presents a comprehensive analysis of the global and regional markets for Biochar in Agriculture, covering the period from 2025 to 2032. It includes detailed insights into the current market status and outlook across various regions and countries, with specific focus on:

● Sales, sales volume, and revenue forecasts

● Detailed segmentation by type and application

The report features in-depth competitive intelligence including:

● Market share analysis of leading manufacturers

● Production capacity expansions

● Product portfolio assessments

● Strategic partnership evaluations

Our research methodology combines primary interviews with industry leaders and comprehensive data analysis of:

● Production facilities and their geographical distribution

● Raw material sourcing patterns

● End-user industry consumption trends

● Regulatory impact assessments

Get Full Report Here: https://www.24chemicalresearch.com/reports/284790/global-aluminum-plate-sheet-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

● Plant-level capacity tracking

● Real-time price monitoring

● Techno-economic feasibility studies

With a dedicated team of researchers possessing over a decade of experience, we focus on delivering actionable, timely, and high-quality reports to help clients achieve their strategic goals. Our mission is to be the most trusted resource for market insights in the chemical and materials industries.

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/