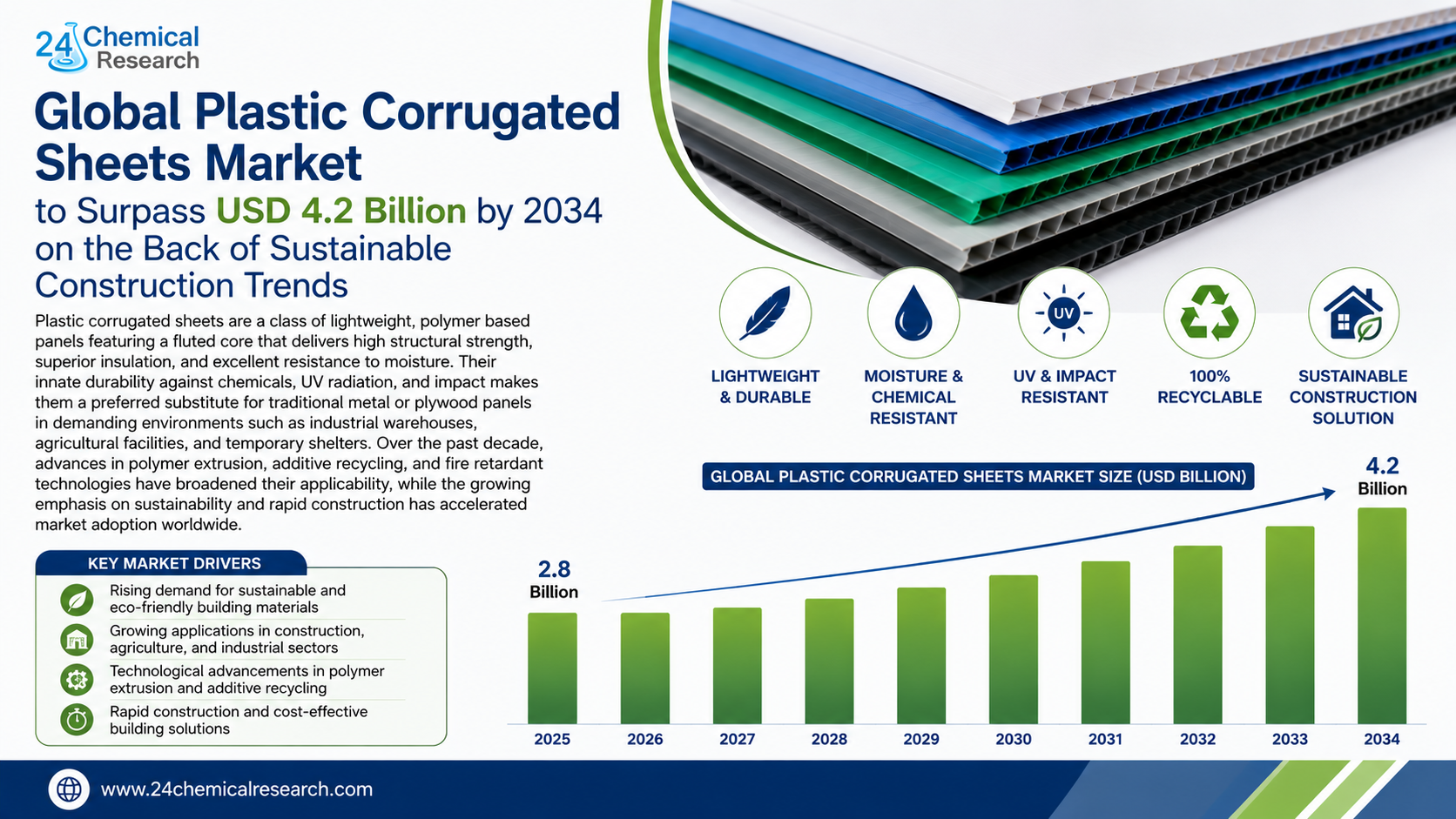

Global Plastic Corrugated Sheets Market to Surpass USD 4.2 Billion by 2034 on the Back of Sustainable Construction Trends

Plastic corrugated sheets are a class of lightweight, polymer‑based panels featuring a fluted core that delivers high structural strength, superior insulation, and excellent resistance to moisture. Their innate durability against chemicals, UV radiation, and impact makes them a preferred substitute for traditional metal or plywood panels in demanding environments such as industrial warehouses, agricultural facilities, and temporary shelters. Over the past decade, advances in polymer extrusion, additive recycling, and fire‑retardant technologies have broadened their applicability, while the growing emphasis on sustainability and rapid construction has accelerated market adoption worldwide.

Get Full Report Here: https://www.24chemicalresearch.com/reports/316871/plastic-corrugated-sheets-market

Market Dynamics:

The market's trajectory is shaped by a complex interplay of powerful growth drivers, significant restraints that are being actively addressed, and vast, untapped opportunities.

Powerful Market Drivers Propelling Expansion

- Surging Construction Activity and Modular Building Trends: The global construction sector, estimated to exceed $12 trillion in annual spend, continues to demand fast‑assembly, cost‑effective, and low‑maintenance materials. Plastic corrugated sheets meet these criteria by offering a 30‑40% reduction in handling weight compared with steel, which translates into faster erection times and lower labor costs. Moreover, their ability to be cut, drilled, and folded on‑site allows contractors to adapt designs quickly, a hallmark of modular and prefabricated building approaches that are gaining momentum across North America, Europe, and emerging Asian economies.

- Environmental and Regulatory Incentives Driving Sustainable Materials: Governments in the European Union, United States, and Canada have introduced stringent waste‑reduction and recycling targets for construction‑grade polymers. In response, manufacturers are increasing the recycled‑content share-often exceeding 30%-in corrugated panels, thereby reducing virgin resin consumption and carbon footprints. The lifecycle‑assessment data released by leading industry bodies show that a high‑recycled‑content sheet can cut greenhouse‑gas emissions by up to 25% relative to a virgin‑polypropylene equivalent, an advantage that resonates with architects seeking green‑building certifications such as LEED and BREEAM.

- Technological Innovations Enhancing Performance and Safety: Recent breakthroughs in polymer chemistry have yielded fire‑retardant additives that achieve UL‑94 V‑0 compliance without sacrificing mechanical strength. Simultaneously, nano‑coating technologies now provide moisture‑barrier performance comparable to traditional metal roofing while preserving the inherent flexibility of the sheet. These innovations open new application windows in sectors where fire safety and moisture protection are paramount, including cold‑storage facilities, pharmaceutical warehouses, and offshore platforms.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/316871/plastic-corrugated-sheets-market

Significant Market Restraints Challenging Adoption

Despite its many advantages, the market faces hurdles that must be overcome to achieve universal adoption.

- Cost Competitiveness with Conventional Materials: While the total cost of ownership for plastic corrugated sheets is favorable over a product’s lifecycle, the upfront material price can still be higher than bulk steel or fiberboard, especially in regions where petrochemical feedstock costs are volatile. This price gap is most pronounced in low‑margin infrastructure projects, where procurement committees often prioritize short‑term cost over long‑term performance benefits.

- Performance Perception and Long‑Term Durability Concerns: Stakeholders occasionally question the long‑term UV stability and thermal expansion characteristics of polymer panels, prompting additional testing requirements and certification delays. Although manufacturers have introduced UV‑stabilizers and reinforcement meshes, the perception gap remains a barrier in highly regulated markets such as Europe and North America.

Critical Market Challenges Requiring Innovation

The transition from prototype to large‑scale production presents technical challenges. Maintaining consistent wall thickness and fluting geometry across high‑speed extrusion lines demands precise temperature control and die design, yet variations of up to ±5% are still reported in certain facilities. In addition, achieving seamless joint integrity for large panels requires advanced sealing systems; otherwise, water ingress can compromise the structure over time. These engineering challenges compel manufacturers to invest heavily in R&D, often allocating 12‑15% of annual revenue to process improvements, automation, and material science research.

Furthermore, the supply chain for virgin polymer granules is fragmented, with price volatility driven by fluctuating crude oil markets (price swings of 20‑30% over the past five years). While recycled‑content strategies mitigate some exposure, scaling closed‑loop recycling to meet rising demand remains an industry‑wide imperative.

Vast Market Opportunities on the Horizon

- Expansion into Emerging Economies and Affordable Housing Initiatives: Rapid urbanization in Southeast Asia, Africa, and Latin America is spurring government‑backed programs aimed at delivering low‑cost, durable housing for millions of families. Plastic corrugated sheets, with their lightweight nature and ease of transport, align perfectly with these initiatives. By establishing localized extrusion plants that tap into regional post‑consumer plastic streams, manufacturers can reduce logistics costs by up to 30% and capture a growing share of the affordable‑housing market.

- Advanced Barrier Versions for Cold‑Chain and Food‑Safety Applications: The food‑logistics sector increasingly demands packaging that limits moisture transmission while remaining lightweight. Recent polymer barrier formulations achieve water vapor transmission rates below 0.3 g/m²·day, enabling thinner sheet profiles without sacrificing protection. Early adopters in the refrigerated transport segment have reported a 12% reduction in product spoilage, highlighting a clear value proposition for broader rollout.

- Strategic Partnerships with Building‑Material Distributors and Digital‑Platform Providers: Collaboration between sheet manufacturers, large‑scale distributors, and emerging construction‑tech platforms is accelerating market penetration. Integrated ordering systems, real‑time inventory visibility, and on‑demand customization tools are shortening lead times and reducing order‑to‑delivery cycles by an average of 25%, a competitive edge that is especially valuable in fast‑paced project environments.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into Polypropylene Corrugated Sheets, Polyethylene Corrugated Sheets, and other specialty polymer variants. Polypropylene Corrugated Sheets currently dominate due to their balanced blend of flexibility, impact resistance, and cost‑effectiveness. Polyethylene variants, while offering superior chemical resistance, are gaining traction in applications requiring higher moisture barriers, such as agricultural mulch and industrial containment.

By Application:

Application segments include Packaging, Construction, Agriculture, and Others. Construction Applications are the largest driver, accounting for the majority of volume because of the material’s suitability for roofing, wall cladding, and temporary structures. Packaging remains a fast‑growing niche, especially for protective secondary packaging where lightweight protection and printable surfaces add brand value. Agricultural uses-such as greenhouse coverings and silo linings-are expanding as farmers seek durable, UV‑stable alternatives to glass and metal.

By End‑User Industry:

The end‑user landscape encompasses the Food & Beverage Industry, Automotive Industry, Consumer Goods, and other sectors. Food & Beverage Industry leverages the hygienic, moisture‑resistant properties of corrugated sheets to protect perishable goods during transport and storage. Automotive suppliers use the panels for interior trim and lightweight cargo solutions, while consumer‑goods manufacturers appreciate the ease of printing custom graphics for promotional displays.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/316871/plastic-corrugated-sheets-market

Competitive Landscape:

The global Plastic Corrugated Sheets market is semi‑consolidated, with a handful of vertically integrated manufacturers controlling polymer extrusion, sheet conversion, and distribution networks. The top three companies-Plastic Corrugated Roofing (PCR) (U.S.), Plastics International Ltd. (China), and Statco Building Products (Canada)-collectively command approximately 55% of the market share as of 2024. Their dominance stems from long‑term resin supply agreements, extensive product portfolios ranging from standard 3 mm gauges to UV‑stabilised fire‑rated grades, and established logistics capabilities that enable rapid delivery to construction sites worldwide.

List of Key Plastic Corrugated Sheets Companies Profiled:

- Plastic Corrugated Roofing (PCR) (United States)

- Plastics International Ltd. (China)

- Statco Building Products (Canada)

- Poly‑Guard Products (United States)

- CorrPro Manufacturing (Philippines)

- Dura‑Last Plastics (United Kingdom)

- Yueyang Plastic Engineering (China)

- National Plastic Roofing Corp. (Australia)

- Supreme Plastic Industries (India)

- Vertic Technology (United Arab Emirates)

Regional Analysis: A Global Footprint with Distinct Leaders

- North America: Is the undisputed leader, holding a 55% share of the global market. Strong demand from residential and commercial construction, coupled with robust recycling infrastructure and stringent building‑code requirements, fuels growth. The United States remains the primary engine, with the Midwest and Sun Belt regions showing the highest per‑capita adoption rates.

- Europe & China: Together, they form a powerful secondary bloc, accounting for 41% of the market. Europe’s growth is driven by EU sustainability directives and the proliferation of modular housing projects in Germany, France, and the Netherlands. China’s market expansion is underpinned by massive urban‑infrastructure programs, a rapidly scaling polymer manufacturing base, and government incentives for recycled‑content construction materials.

- Asia‑Pacific (ex‑China), South America, and MEA: These regions represent emerging frontiers. While currently smaller in scale, they present significant long‑term opportunities fueled by rapid industrialization, rising middle‑class consumption, and increasing infrastructure investments. Countries such as Vietnam, Brazil, and Kenya are poised to become new hubs for localized sheet production as they adopt greener building standards.

Get Full Report Here: https://www.24chemicalresearch.com/reports/316871/plastic-corrugated-sheets-market

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/316871/plastic-corrugated-sheets-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data‑driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

- Plant-level capacity tracking

- Real‑time price monitoring

- Techno‑economic feasibility studies

Contact: +91 9169162030

Website: https://www.24chemicalresearch.com/