Turkey Green Chemicals Market to Grow at 5.5% CAGR Amid Expanding Adoption of Low-Carbon Chemical Technologies

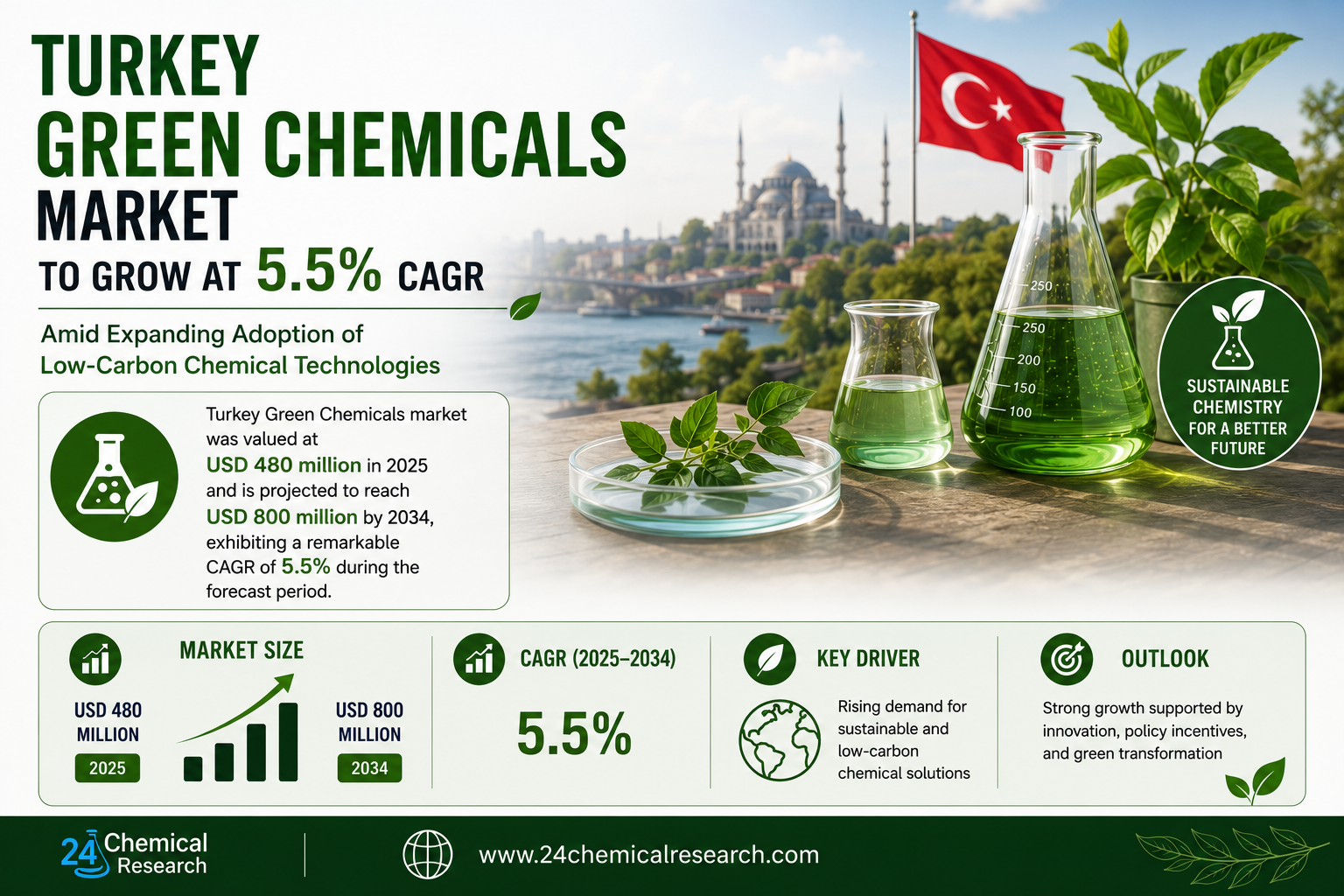

Turkey Green Chemicals market was valued at USD 480 million in 2025 and is projected to reach USD 800 million by 2034, exhibiting a remarkable CAGR of 5.5% during the forecast period.

Green chemicals, encompassing bio‑based solvents, biodegradable surfactants, renewable polymers and natural pigments, have transitioned from niche research projects to mainstream industrial solutions. Their distinctive attributes-low‑toxicity, reduced carbon footprint, and compatibility with existing process lines-make them indispensable for a wide range of applications, from agricultural formulations to high‑performance coatings. Unlike conventional petro‑chemical intermediates, these materials can be processed in aqueous media, allowing seamless integration into production streams while meeting ever‑tighter environmental regulations.

Get Full Report Here: https://www.24chemicalresearch.com/reports/316617/turkey-green-chemicals-market

Market Dynamics:

The market's trajectory is shaped by a complex interplay of powerful growth drivers, significant restraints that are being actively addressed, and vast, untapped opportunities.

Powerful Market Drivers Propelling Expansion

- Sustainable Agriculture and Crop Protection: Turkey’s large agrarian base is driving demand for bio‑based agro‑chemicals that enhance yields while minimizing soil and water contamination. The national push toward integrated pest management, supported by the Ministry of Agriculture, has resulted in a 12% annual increase in adoption of green herbicides and biopesticides. Farmers are increasingly turning to plant‑derived surfactants and microbial inoculants, which reduce dependence on synthetic chemicals and align with EU export standards for pesticide residues.

- Eco‑Friendly Manufacturing in Automotive and Textiles: Key Turkish industries such as automotive parts suppliers and textile manufacturers are under pressure to meet EU‑type emissions targets. By substituting traditional solvents with bio‑based alternatives, these sectors achieve up to 15% reductions in volatile organic compound (VOC) emissions. Major OEMs are incorporating green polymers into lightweight components, which not only cut vehicle weight but also qualify for green‑vehicle incentives in the European market.

- Circular‑Economy Initiatives and Waste Valorisation: Government‑backed circular‑economy programmes encourage the conversion of agricultural residues-wheat straw, olive pomace and hazelnut shells-into platform chemicals. Pilot plants in the Thrace region have demonstrated conversion yields of 68%, rivaling imported corn‑derived feedstocks. This feedstock diversification reduces import reliance and provides a stable cost base for green‑chemical producers.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/316617/turkey-green-chemicals-market

Significant Market Restraints Challenging Adoption

Despite its promise, the market faces hurdles that must be overcome to achieve universal adoption.

- High Capital Expenditure for Green Plants: Constructing dedicated bio‑based production facilities requires significant upfront investment in specialized reactors, downstream purification units and certification processes. According to industry surveys, capital costs can be 20‑30% higher than for conventional petro‑chemical upgrades, deterring smaller firms despite strong demand signals.

- Regulatory Ambiguities and Certification Lag: While Turkey aligns its chemical regulations with EU REACH and CLP frameworks, the approval timeline for novel bio‑based substances can extend beyond 24 months. This lag creates uncertainty for manufacturers who must balance time‑to‑market against compliance risk, especially for high‑value consumer‑goods applications.

Critical Market Challenges Requiring Innovation

Scaling laboratory‑scale bioprocesses to industrial volumes remains a technical bottleneck. Many producers report yield variability of 10‑15% when moving from pilot batches of 5 tons to commercial runs exceeding 100 tons per day. Moreover, downstream separation of bio‑derived intermediates often relies on energy‑intensive chromatography, which inflates operating costs. Overcoming these challenges demands sustained R&D investment-often 12‑18% of annual revenue for leading firms-and the development of continuous flow technologies that promise higher consistency and lower energy consumption.

Additionally, the supply chain for renewable feedstocks is still fragmented. Seasonal fluctuations in agricultural residue availability, coupled with price volatility of imported corn‑based glucose (which can swing 8‑12% YoY), introduce risk for long‑term contracts. Until robust feedstock aggregation platforms emerge, manufacturers will continue to hedge against supply disruptions, impacting price stability for end customers.

Vast Market Opportunities on the Horizon

- Advanced Water‑Treatment Solutions: Green chemicals such as bio‑based coagulants, biodegradable membranes and enzyme‑enhanced filtration media are poised to disrupt the $90 billion global water‑treatment market. Early field trials in the Marmara region have shown a 30‑40% reduction in chemical dosing compared with conventional aluminium sulphate, while maintaining over 99% contaminant removal efficiency. With Turkey’s strategic position as a water‑resource hub for the Balkans and the Middle East, domestic manufacturers could capture a sizable export niche.

- High‑Performance Coatings for Marine and Infrastructure: Innovative bio‑based anti‑corrosion paints and self‑healing epoxy systems are gaining traction in Turkey’s expanding offshore wind farm projects. Laboratory data indicate a 20‑25% extension in coating lifespan compared with traditional solvent‑borne systems, translating into lower maintenance budgets for operators and a compelling value proposition for public‑private infrastructure partnerships.

- Strategic Partnerships and Open‑Innovation Platforms: Over the past three years, more than 45 collaborative agreements have been signed between Turkish chemical firms and European research institutes. These partnerships accelerate technology transfer, reduce time‑to‑market by an estimated 35%, and spread R&D risk. As a result, joint‑development pipelines are delivering next‑generation biodegradable polymers ready for automotive interior components and packaging applications.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into Bio‑based solvents, Biodegradable surfactants, Green polymers and Natural pigments. Bio‑based solvents currently lead the market, favored for their easy integration into existing process equipment, low VOC profile and versatility across sectors ranging from textile dyeing to pharmaceutical intermediates. Green polymers, while still a smaller share, are rapidly gaining traction for applications in biodegradable packaging and automotive interior parts.

By Application:

Application segments include Agricultural chemicals, Textile processing, Cleaning products, Personal‑care cosmetics and Others. Cleaning products represent a pivotal application segment for green chemicals in Turkey. Consumers and institutional buyers alike are gravitating toward formulations that avoid hazardous phosphates and volatile organic compounds, preferring solutions derived from plant‑based surfactants and enzymatic boosters. This demand is fueling collaborations between local chemical firms and multinational brands to develop biodegradable cleaners that deliver comparable efficacy to conventional counterparts.

By End User:

The end‑user landscape includes Industrial manufacturers, Consumer‑goods companies, Agricultural cooperatives and Government agencies. Industrial manufacturers are the leading end‑user driving the expansion of Turkey’s green chemicals market. These firms are integrating environmentally responsible inputs into their production lines to meet stricter EU‑aligned regulations and to respond to corporate sustainability road‑maps. By substituting traditional petrochemical intermediates with green alternatives, manufacturers achieve lower emissions, reduced waste generation and enhanced brand credibility.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/316617/turkey-green-chemicals-market

Competitive Landscape:

The Turkey Green Chemicals market is semi‑consolidated and characterized by intense competition and rapid innovation. The top four companies-Petkim, BASF Turkey, AkzoNobel Turkey and Ceylan Holding-collectively command approximately 55% of the market share as of 2024. Their dominance is underpinned by extensive R&D pipelines, integrated production facilities and established distribution networks across Europe and the Middle East.

List of Key Turkey Green Chemicals Companies Profiled:

- Petkim (Turkey)

- BASF Turkey (Turkey)

- AkzoNobel Turkey (Turkey)

- Ceylan Holding (Turkey)

- Novamont Turkey (Turkey)

- GreenTech Solutions (Turkey)

- ENIQ Chemicals (Turkey)

- Zirve BioChem (Turkey)

Regional Analysis: A Global Footprint with Distinct Leaders

- Europe: Remains the largest export destination for Turkish green chemicals, accounting for roughly 45% of total outbound shipments. Alignment with EU REACH and CLP regulations facilitates market access, while demand for low‑VOC solvents and biodegradable polymers drives premium pricing.

- Middle East & North Africa (MENA): Identified as an emerging market, MENA countries are investing heavily in water‑treatment infrastructure and sustainable construction, creating strong demand for bio‑based coagulants, anti‑corrosion coatings and renewable polymer binders.

- Central Asia: Shows the fastest growth in domestic consumption, propelled by government incentives for circular‑economy projects and a burgeoning agro‑processing sector that seeks locally sourced bio‑based inputs.

Get Full Report Here: https://www.24chemicalresearch.com/reports/316617/turkey-green-chemicals-market

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/316617/turkey-green-chemicals-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data‑driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

- Plant-level capacity tracking

- Real-time price monitoring

- Techno-economic feasibility studies

Contact: +91 9169162030

Website: https://www.24chemicalresearch.com/