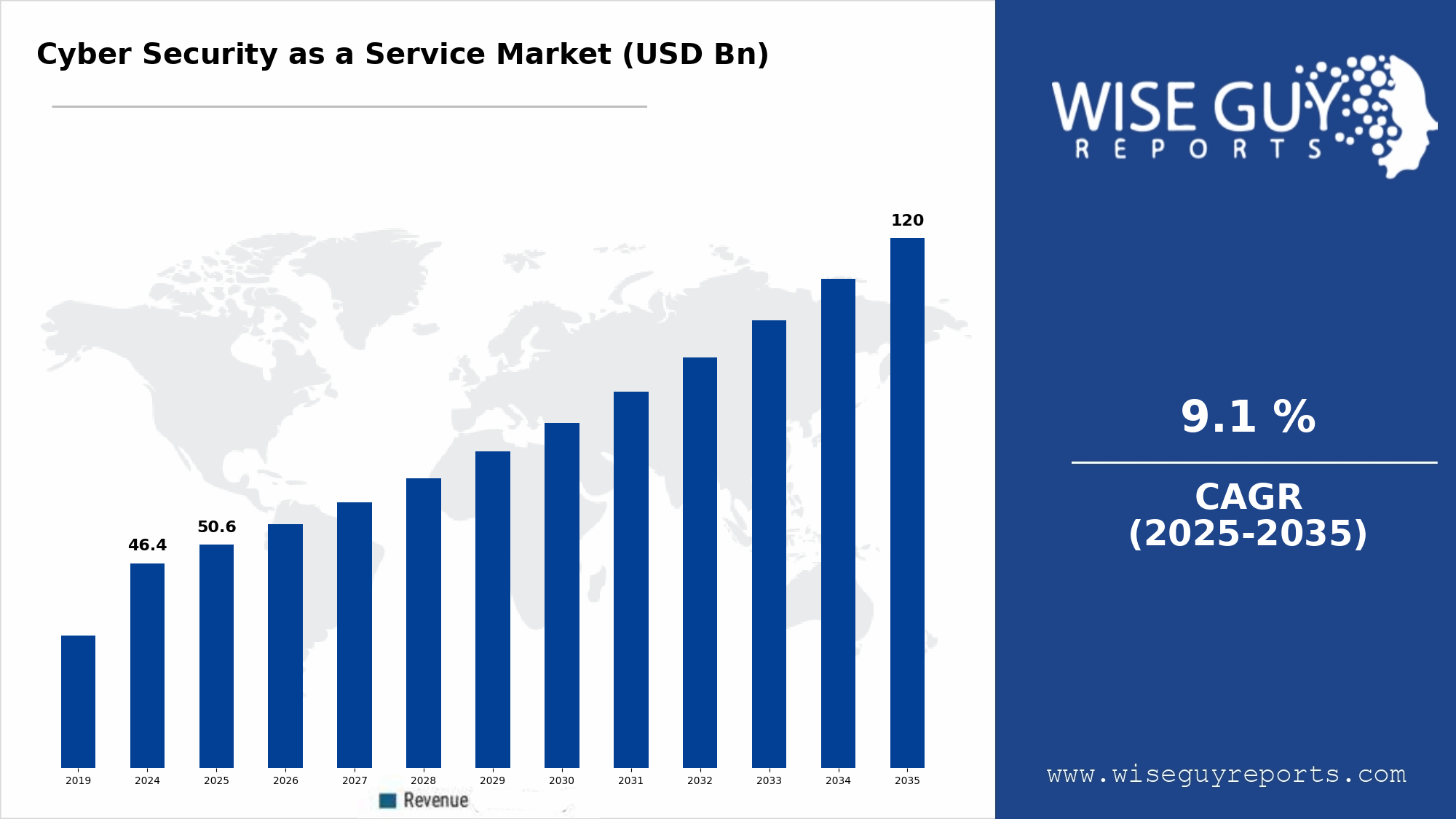

The Cyber Security as a Service Market is expected to grow from 50.6 USD Billion in 2025 to 120 USD Billion by 2035. The Cyber Security as a Service Market CAGR (growth rate) is expected to be around 9.1% during the forecast period (2025 - 2035). This sustained expansion signals a fundamental redefinition of enterprise cybersecurity, where managed, intelligence-led services are replacing siloed, tool-based defense strategies. Organizations are increasingly prioritizing resilience, visibility, and rapid response over static protection models that struggle to keep pace with evolving threats.

The transformation of the Cyber Security as a Service Market is being shaped by enterprises seeking continuous protection across hybrid IT environments. As business operations span cloud platforms, SaaS applications, remote endpoints, and third-party ecosystems, the need for unified, service-driven security frameworks has become critical. Cybersecurity services now function as an extension of enterprise governance rather than a standalone IT function.

Strategic Market Evolution and Demand Patterns

One of the most defining characteristics of the market is the transition from reactive security to proactive threat management. Organizations are demanding services that not only detect breaches but also anticipate them through predictive analytics and behavioral intelligence. This evolution is driven by the growing sophistication of cyber adversaries, who increasingly rely on automation, social engineering, and supply-chain vulnerabilities.

Another important trend shaping demand is the growing emphasis on business continuity and operational resilience. Cyber incidents are no longer viewed solely as IT disruptions; they are enterprise-wide risks with financial, reputational, and regulatory consequences. As a result, cybersecurity services are being integrated into broader risk management and compliance strategies.

Key Players and Recent Developments

The competitive landscape is led by established technology vendors and specialized managed security service providers. Companies such as IBM Security, Cisco Systems, Palo Alto Networks, Fortinet, Broadcom (Symantec), Trend Micro, and AT&T Cybersecurity continue to invest heavily in automation, artificial intelligence, and extended detection and response capabilities.

Recent developments highlight a strong focus on platform consolidation and AI-driven analytics. IBM has expanded its managed detection and response offerings by embedding advanced threat intelligence and automated remediation into its security operations services. Palo Alto Networks has strengthened its cloud-native security portfolio through AI-powered analytics, while Cisco continues to enhance its integrated security ecosystem to improve cross-domain visibility. These initiatives reflect a broader industry move toward unified security platforms delivered as a service.

Detailed Market Segmentation

The Cyber Security as a Service Market can be segmented by service type, deployment model, organization size, and industry vertical. By service type, managed detection and response, managed SIEM, managed IAM, managed endpoint protection, and managed compliance services represent the core offerings. Managed detection and response services are gaining the strongest traction, as they address the critical need for real-time threat identification and rapid mitigation.

From a deployment perspective, cloud-based services dominate due to their scalability, continuous updates, and cost efficiency. Hybrid deployments are also gaining relevance among enterprises that maintain sensitive workloads on-premises while leveraging cloud-based security intelligence.

When segmented by organization size, large enterprises continue to account for a significant share due to complex infrastructures and regulatory exposure. However, small and medium-sized enterprises are emerging as a high-growth segment, driven by subscription-based pricing models that make advanced security capabilities accessible without large upfront investments.

Dominating Regional Landscape

North America remains the dominant region in the Cyber Security as a Service Market, supported by advanced digital infrastructure, high cybersecurity spending, and early adoption of managed security models. The United States, in particular, benefits from a dense ecosystem of cybersecurity vendors and strong regulatory enforcement.

Europe follows closely, with regulatory frameworks such as GDPR and NIS2 compelling organizations to adopt comprehensive security services. Asia Pacific is expected to witness the fastest growth, fueled by rapid digitalization, expanding cloud adoption, and increasing cyber risk awareness across emerging economies.

FAQs

-

Why are enterprises shifting toward cybersecurity services instead of in-house tools?

Enterprises value the continuous monitoring, expert oversight, and scalability that service-based models provide, especially amid growing skill shortages. -

Which service segment is expected to grow fastest?

Managed detection and response services are projected to see strong growth due to rising threat complexity. -

Is data privacy a concern with managed services?

Leading providers address this through robust compliance frameworks, encryption, and localized data governance models.