The automotive landscape is undergoing a radical shift as vehicles transition from simple transport machines to sophisticated, data-driven platforms. The rise of connected and autonomous vehicles (CAVs) has created an unprecedented demand for high-capacity and high-speed memory solutions. As vehicles integrate more sensors, cameras, and communication modules, the need for reliable storage and processing power becomes a fundamental requirement for the next generation of mobility.

Market Growth and Valuation Projections

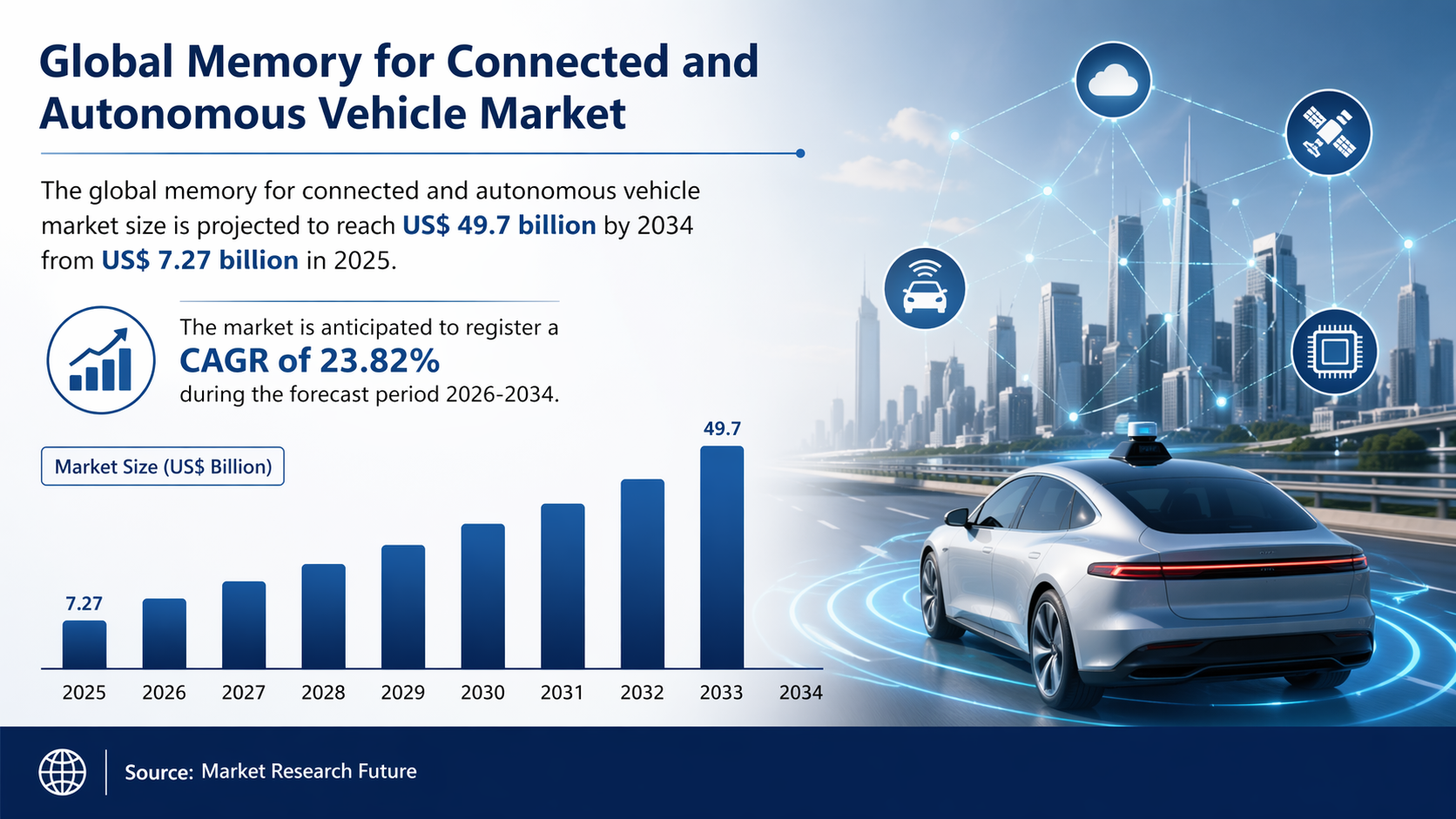

The expansion of electronic content in vehicles is the primary driver behind the rapid financial growth of this sector. According to recent industry data, the global memory for connected and autonomous vehicle market size is projected to reach US$ 49.7 billion by 2034 from US$ 7.27 billion in 2025. The market is anticipated to register a CAGR of 23.82% during the forecast period 2026-2034. This significant growth reflects the shift toward Level 3 and Level 4 autonomy, where real-time data processing and safety-critical storage are paramount.

Comprehensive Report Segmentation Analysis

To understand the diverse needs of the automotive sector, a detailed Memory for Connected and Autonomous Vehicle Market Segmentation is essential. The market is categorized based on component types, including DRAM, NAND Flash, NOR Flash, and SRAM. DRAM is particularly vital for real-time processing in Advanced Driver Assistance Systems (ADAS), while NAND Flash provides the high-density storage required for complex operating systems and high-definition mapping data.

Furthermore, the market is segmented by application areas such as Infotainment, ADAS and Autonomous Driving, Telematics, and Digital Instrument Clusters. The ADAS segment is expected to hold a dominant share as automakers prioritize safety features like lane-keeping assistance, adaptive cruise control, and automated emergency braking. Each of these applications demands different performance characteristics, ranging from low latency to high endurance in harsh environmental conditions.

Drivers of Advanced Memory Adoption

The move toward software-defined vehicles is a major catalyst for memory adoption. Modern vehicles require massive amounts of code to manage everything from battery efficiency to cabin climate. Additionally, the integration of 5G technology enables Vehicle-to-Everything (V2X) communication, which generates a continuous stream of data that must be buffered and stored. This environment necessitates memory that can handle high write-cycle endurance and maintain data integrity over the long lifespan of a vehicle.

Download Sample Report: https://www.theinsightpartners.com/sample/TIPRE00010520

Regional Market Dynamics

Geographically, the demand is distributed across major automotive hubs. North America and Europe are leading the way in the deployment of luxury autonomous vehicles, while the Asia Pacific region, particularly China, is seeing a surge in mass-market electric vehicles equipped with advanced connectivity features. Local government regulations regarding vehicle safety and data privacy are also influencing how memory solutions are implemented in different jurisdictions.

Key Players in the Global Market

The industry is supported by a group of specialized semiconductor manufacturers who focus on automotive-grade reliability. These key players include:

-

ATP Electronics, Inc.

-

Cypress Semiconductor Corporation

-

Everspin Technologies Inc.

-

Integrated Silicon Solution Inc.

-

MACRONIX (HONG KONG) CO., LTD.

-

Microchip Technology Inc.

-

Micron Technology, Inc.

-

Nanya Technology Corporation

-

Renesas Electronics Corporation

-

SK HYNIX INC.

Challenges in Automotive Memory Implementation

Despite the positive growth outlook, the industry faces challenges such as the need for extreme temperature resistance and vibration durability. Automotive memory must operate reliably between -40 degrees Celsius and +125 degrees Celsius. Ensuring functional safety through certifications like ISO 26262 is a rigorous process that requires significant investment from chipmakers. Furthermore, the global semiconductor supply chain volatility remains a factor that manufacturers must navigate to meet the rising demand.

Future Outlook

The future of the memory market for connected and autonomous vehicles is intrinsically linked to the evolution of Artificial Intelligence at the edge. As AI algorithms become more localized within the vehicle to reduce latency, the demand for high-bandwidth memory like LPDDR5 and GDDR6 will increase. We expect to see a move toward more integrated storage architectures that can handle the massive data throughput of multiple 8K cameras and LiDAR sensors simultaneously. As the industry approaches 2034, memory will no longer be a peripheral component but the core foundation upon which autonomous mobility is built, ensuring that vehicles are not only connected but also intelligent and safe.

Related Reports:

About Us

The Insight Partners is a leading global market research and consulting firm specializing in delivering actionable insights across various industries. Our research reports combine extensive primary and secondary research to provide accurate market intelligence, helping businesses make informed strategic decisions. The company provides detailed analysis on emerging technologies, market trends, competitive landscapes, and growth opportunities across sectors including technology, healthcare, manufacturing, and energy.

Contact Us:

Contact Person: Ankit Mathur

E-mail: ankit.mathur@theinsightpartners.com

Phone: +1-646-491-9876