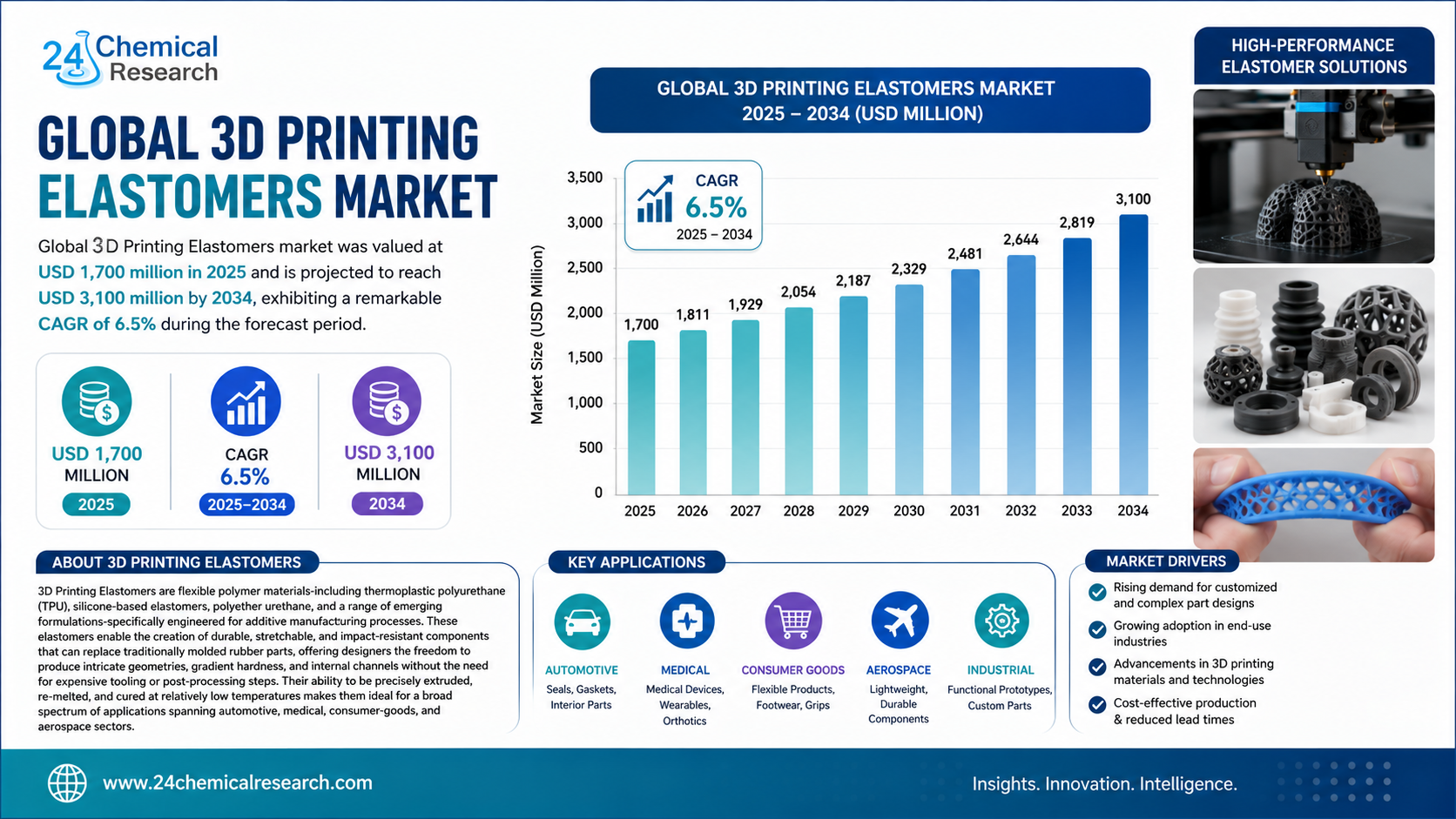

Global 3D Printing Elastomers market was valued at USD 1,700 million in 2025 and is projected to reach USD 3,100 million by 2034, exhibiting a remarkable CAGR of 6.5% during the forecast period.

3D Printing Elastomers are flexible polymer materials-including thermoplastic polyurethane (TPU), silicone‑based elastomers, polyether urethane, and a range of emerging formulations-specifically engineered for additive manufacturing processes. These elastomers enable the creation of durable, stretchable, and impact‑resistant components that can replace traditionally molded rubber parts, offering designers the freedom to produce intricate geometries, gradient hardness, and internal channels without the need for expensive tooling or post‑processing steps. Their ability to be precisely extruded, re‑melted, and cured at relatively low temperatures makes them ideal for a broad spectrum of applications spanning automotive, medical, consumer‑goods, and aerospace sectors.

Get Full Report Here: https://www.24chemicalresearch.com/reports/316840/d-printing-elastomers-market

Market Dynamics:

The market's trajectory is shaped by a complex interplay of powerful growth drivers, significant restraints that are being actively addressed, and vast, untapped opportunities. While demand for lightweight, flexible components is surging, manufacturers must simultaneously navigate capital intensity, regulatory scrutiny, and supply‑chain fragmentation to fully capitalise on the technology's potential.

Powerful Market Drivers Propelling Expansion

-

Lightweight Automotive & Aerospace Applications: The automotive and aerospace sectors are under relentless pressure to reduce weight and improve fuel efficiency, and elastomeric 3D‑printed components are emerging as a practical solution. Flexible seals, vibration‑damping mounts, and interior trim pieces fabricated from TPU or silicone elastomers can achieve up to 30% weight reduction compared with conventional rubber, while preserving tensile strengths above 20 MPa and excellent abrasion resistance. These gains translate directly into lower emissions and longer service intervals, aligning with stringent regulatory targets and the industry's strategic roadmap for next‑generation vehicle platforms.

-

Personalised Medical Devices and Wearable Health Technology: Regulatory agencies have recently clarified pathways for patient‑specific elastomeric implants, encouraging medical device manufacturers to adopt additive manufacturing for rapid prototyping and low‑volume production. TPU and silicone filaments enable the fabrication of custom prosthetic liners, soft surgical guides, and wearable health monitors that conform precisely to individual anatomy. Speed to market improves dramatically-engineers can iterate a design in days rather than weeks-while the ability to produce on‑demand parts reduces inventory costs and waste. Recent industry surveys indicate that more than 40% of leading medical‑device firms now view elastomeric 3D printing as a strategic capability.

-

Multi‑Material Additive Manufacturing Platforms: Advanced industrial printers that can switch between rigid polymers and elastomers within a single build are unlocking new product architectures. By synchronising extrusion temperatures, pressure profiles, and material feed rates, manufacturers can embed flexible joints directly into structural components, eliminating secondary assembly operations and reducing part counts. This integration yields lead‑time reductions of approximately 25% for low‑volume, custom‑fit assemblies and drives material waste down to less than 3% of the build volume, delivering both economic and environmental benefits.

Download FREE Sample Report: 3D Printing Elastomers Market - View in Detailed Research Report

Significant Market Restraints Challenging Adoption

Despite its promise, the market faces hurdles that must be overcome to achieve universal adoption across all target industries.

-

High Capital Expenditure for Specialized Equipment: Printers capable of maintaining heated build chambers above 200 °C, delivering filament diameters with tolerances of ±0.02 mm, and providing precise extrusion force for viscous elastomer melts require substantial upfront investment. For many small‑ and medium‑sized enterprises, the capital outlay for such equipment-often exceeding $500,000-creates a barrier to entry, slowing diffusion of elastomeric additive manufacturing beyond large, well‑funded OEMs.

-

Regulatory and Certification Complexities: Medical, aerospace, and automotive applications demand rigorous validation of material biocompatibility, fire‑retardancy, and long‑term mechanical stability. Certification processes can extend from 12 to 24 months, involving extensive testing, documentation, and audit trails. The associated time and cost pressures discourage some manufacturers from adopting new elastomer formulations without clear, pre‑approved pathways.

Critical Market Challenges Requiring Innovation

The transition from laboratory formulations to high‑volume industrial production introduces several technical challenges. Maintaining uniform filament viscosity across batches is difficult, especially for silicone‑based elastomers that are sensitive to trace moisture. Inconsistent rheology can lead to nozzle clogging, layer delamination, and surface defects, which are unacceptable for safety‑critical parts. Additionally, printed elastomer components often require post‑processing-such as UV curing, annealing, or solvent‑based surface treatments-to achieve the desired mechanical performance and dimensional stability. These extra steps increase cycle time and operational complexity, prompting the need for integrated process controls, real‑time monitoring, and advanced material chemistries that minimise post‑processing requirements.

Furthermore, the supply chain for high‑performance elastomer resins remains fragmented. A limited number of certified filament manufacturers dominate the market, resulting in price volatility and long lead times for bulk orders. Raw‑material price fluctuations for specialty polymers-driven by feedstock availability and global petrochemical trends-add another layer of uncertainty for end‑users seeking predictable cost structures for large‑scale production runs.

Vast Market Opportunities on the Horizon

-

Flexible Electronics and Wearable Devices: Elastomeric filaments with engineered dielectric constants and low loss tangents are enabling the direct printing of stretchable antennas, conductive traces, and tactile sensors. As the global wearable market approaches $70 billion by 2027, manufacturers that can integrate these functional elastomers into smart garments, health monitors, and flexible displays will capture a rapidly expanding niche that bridges the gap between electronics and textiles.

-

Advanced Automotive Interior & Exterior Parts: The move toward greener, lighter vehicles is driving automakers to explore 3D‑printed elastomeric components for interior dashboards, door panels, and exterior aerodynamic trims that require both flexibility and aesthetic surface finish. Gradient‑hardness designs-where a single part transitions from a soft grip zone to a rigid support structure-enable innovative ergonomics and weight optimisation that traditional injection‑moulded parts cannot match.

-

Strategic Partnerships and Ecosystem Development: Collaboration between material producers, printer OEMs, and end‑user companies has accelerated the qualification of new elastomer grades. Over 40 strategic alliances have been announced in the past three years, spanning joint R&D programs, co‑development of application‑specific formulations, and shared testing facilities. These partnerships reduce development risk, pool investment, and compress time‑to‑market, creating a virtuous cycle that fuels further innovation across the additive manufacturing ecosystem.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The market is segmented into Thermoplastic Polyurethane (TPU) Elastomers, Silicone‑Based Elastomers, Polyether Urethane Elastomers, and Other Emerging Formulations. Thermoplastic Polyurethane (TPU) Elastomers currently lead the market because they provide an optimal balance of Shore hardness, tear resistance, and low processing temperature, making them compatible with widely adopted fused deposition modelling (FDM) platforms. Their re‑meltability supports iterative design cycles, while the inherent chemical resistance and durability address the demanding performance criteria of automotive and consumer‑goods applications.

By Application:

Application segments include Rapid Prototyping of Flexible Components, Custom Tooling and Fixtures, Functional End‑Use Parts, Medical Device Components, and Others. Functional End‑Use Parts represent the most compelling application, as manufacturers seek to replace traditionally moulded rubber components with digitally produced alternatives that can be tailored to precise performance specifications. The ability to embed internal channels, gradient hardness zones, and complex lattice structures within a single print enables designers to achieve weight reductions, part consolidation, and enhanced part‑level functionality that were previously unattainable with conventional manufacturing.

By End‑User Industry:

The end‑user landscape includes Automotive Manufacturing, Healthcare and Medical Devices, and Consumer Electronics. Healthcare and Medical Devices drive a significant portion of demand for elastomeric 3D printing because of strict performance criteria around biocompatibility, softness, and sterilisation resistance. Researchers and device makers value the capacity to produce patient‑specific anatomical models, wearable supports, and soft actuators without extensive tooling investment, accelerating innovation cycles and enabling rapid clinical validation.

Download FREE Sample Report: 3D Printing Elastomers Market - View in Detailed Research Report

Competitive Landscape:

The global 3D Printing Elastomers market is semi‑consolidated and characterised by intense competition and rapid innovation. The top three companies-BASF (Germany), Evonik Industries (Germany), and Dow (USA)-collectively command approximately 55% of the market share as of 2024. Their dominance is underpinned by extensive polymer R&D pipelines, vertical integration that controls resin formulation, quality assurance, and global logistics, and strategic collaborations with leading printer manufacturers. These incumbents leverage economies of scale to offer consistent material quality, while continuously expanding their elastomer portfolios to meet emerging application needs.

List of Key 3D Printing Elastomers Companies Profiled:

-

BASF (Germany)

-

Evonik Industries (Germany)

-

Dow (USA)

-

Covestro (Germany)

-

eSUN (China)

-

Formlabs (USA)

-

3D Systems (USA)

-

Misumi Materials (Japan)

-

Polymaker (China)

-

Henkel (Germany)

The competitive strategy across the sector is overwhelmingly focused on R&D to enhance material performance-such as improving tear resistance, reducing viscosity variability, and developing low‑temperature curing chemistries-while simultaneously forming strategic vertical partnerships with OEMs and service‑bureau providers to co‑develop and validate new applications. This dual focus on innovation and collaboration ensures a steady pipeline of next‑generation elastomeric solutions that meet the evolving demands of high‑value end‑users.

Regional Analysis: A Global Footprint with Distinct Leaders

-

North America: Is the undisputed leader, holding a 55% share of the global market. This dominance is fueled by massive R&D investments from leading polymer manufacturers, a robust network of additive‑manufacturing service bureaus, and strong demand from its world‑leading automotive, aerospace, and medical‑device sectors. The United States serves as the primary engine of growth, with a mature supply chain that can rapidly translate material innovations into production‑ready elastomeric filaments.

-

Europe & China: Together, they form a powerful secondary bloc, accounting for 41% of the market. Europe leverages flagship programmes such as Horizon Europe and the EU’s Polymer Innovation Initiative to fund advanced elastomer research, while Germany’s legacy in high‑performance polymers provides a solid foundation for commercialisation. China, backed by strong governmental incentives and a vast manufacturing base, accelerates adoption in consumer electronics, wearable technology, and mass‑market automotive components, creating a synergistic growth environment across the region.

-

Asia‑Pacific (ex‑China), South America, and MEA: These regions represent the emerging frontier of the elastomers market. Although current market size is modest, they present significant long‑term growth opportunities driven by rapid industrialisation, rising investments in electric‑vehicle production, and growing consumer demand for flexible wearable devices. Localised production hubs, supported by government‑led additive‑manufacturing incubators, are beginning to emerge, laying the groundwork for future market expansion.

Get Full Report Here: https://www.24chemicalresearch.com/reports/316840/d-printing-elastomers-market

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/316840/d-printing-elastomers-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data‑driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

-

Plant‑level capacity tracking

-

Real‑time price monitoring

-

Techno‑economic feasibility studies

Contact: +91 9169162030

Website: https://www.24chemicalresearch.com/