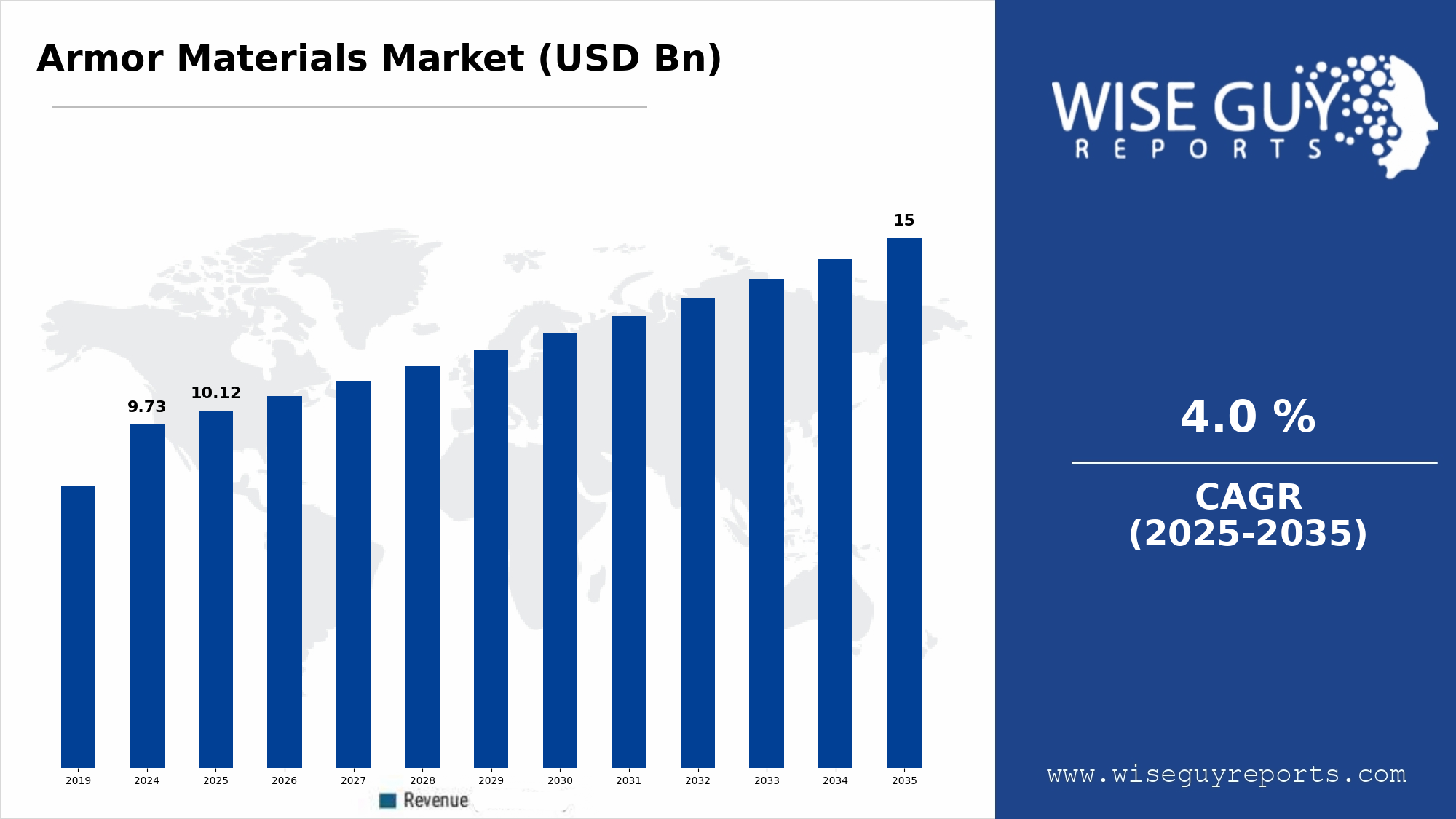

The Armor Materials Market Size was valued at 9.73 USD Billion in 2024. The Armor Materials Market is expected to grow from 10.12 USD Billion in 2025 to 15 USD Billion by 2035. The Armor Materials Market CAGR (growth rate) is expected to be around 4.0% during the forecast period (2025 - 2035).

The global armor materials industry is shaped by the dual priorities of enhanced protection and operational mobility. Modern defense doctrines emphasize soldier survivability, platform agility, and modularity, driving sustained demand for materials that offer superior ballistic resistance without excessive weight penalties. This balance is becoming increasingly critical as armed forces adapt to asymmetric warfare and multi-domain threat environments.

Industry insights from the Armor Materials Market indicate that innovation in materials engineering is central to competitive differentiation. Advanced ceramics and fiber-reinforced composites are increasingly replacing traditional monolithic steel solutions in many applications. These materials not only improve ballistic performance but also support modular armor configurations, enabling forces to tailor protection levels based on mission requirements.

Segmentation by material type highlights metals, ceramics, fibers, and composites as the core categories. Metals such as hardened steel and aluminum alloys continue to dominate heavy vehicle armor due to structural strength and cost efficiency. Ceramics, including alumina and silicon carbide, are critical for defeating high-velocity threats and are widely used in personal armor and vehicle applique systems. Fiber-based materials such as aramid and UHMWPE are essential for soft armor solutions, while composite systems integrate multiple materials to optimize protection and weight.

From an application standpoint, land defense platforms remain the largest consumers of armor materials. Armored vehicles, main battle tanks, and troop carriers account for significant material volumes. Personal protection equipment, including body armor and helmets, represents a consistently strong segment driven by soldier modernization programs. Aerospace and naval applications are smaller but strategically important, particularly for lightweight spall liners and ballistic protection in aircraft and ships.

Regionally, North America maintains a dominant position in the Armor Materials Market, supported by extensive defense budgets, advanced R&D infrastructure, and long-term procurement programs. Europe follows, driven by fleet modernization initiatives and increased defense collaboration. Asia-Pacific is emerging as a high-growth region, fueled by expanding defense expenditures and domestic manufacturing capabilities in countries such as China and India. The Middle East continues to invest heavily in armored platforms and internal security systems, sustaining regional demand.

Leading companies such as DuPont, Saint-Gobain, CeramTec, and ATI are focusing on lightweight solutions, improved multi-hit capability, and sustainable manufacturing. Recent developments include next-generation ceramic strike faces and enhanced fiber architectures designed to improve durability and comfort.

Looking forward, the market is expected to benefit from continuous innovation and increasing emphasis on survivability across defense platforms, supporting steady growth through 2035.

FAQs

- Why are lightweight armor materials important?

They enhance mobility and reduce fatigue while maintaining required protection levels. - Which application segment dominates demand?

Land-based military platforms dominate overall demand. - What regions show the strongest growth potential?

Asia-Pacific and the Middle East show strong growth potential.